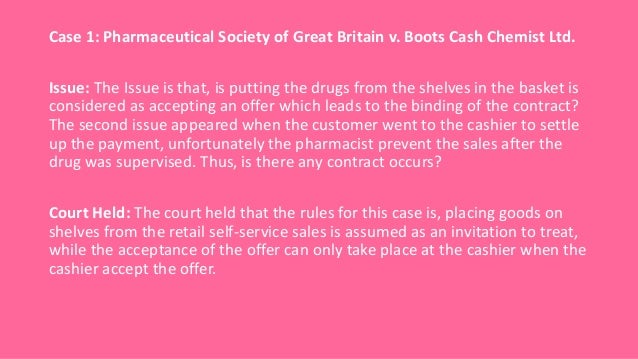

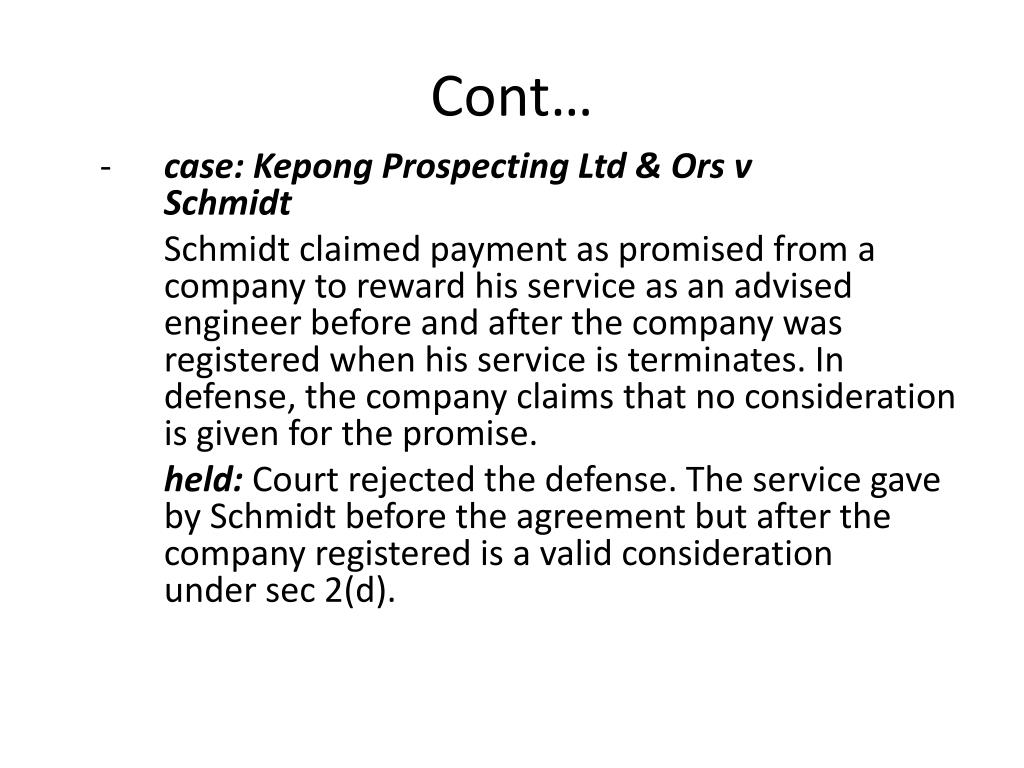

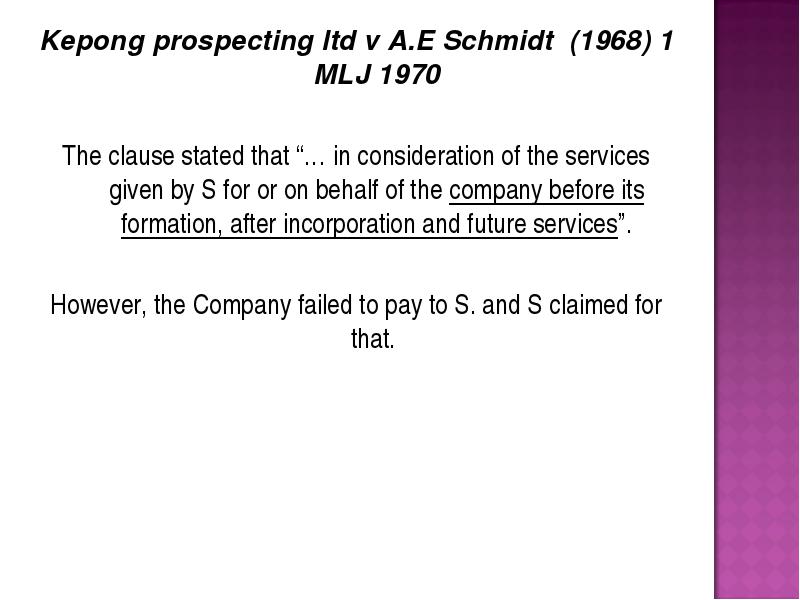

Kepong Prospecting Ltd V Schmidt

Chapter 4 Elements Of Contract Part Ii By Siti Suhaidah Issuu

Madam Norazla Abdul Wahab Ppt Video Online Download

Kepong Prospecting V Schmidt

Question Commercial Law Us

Section 26 Of Ca 1950 Section 26 Of Ca 1950

Ppt Consideration Powerpoint Presentation Free Download Id 3786798

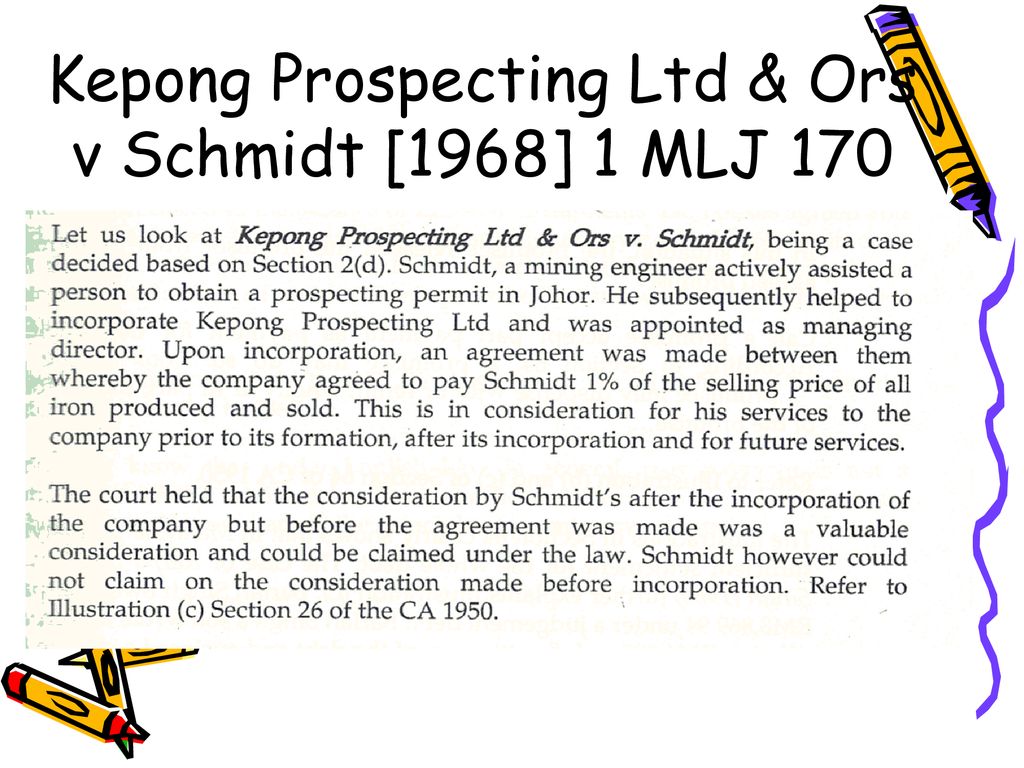

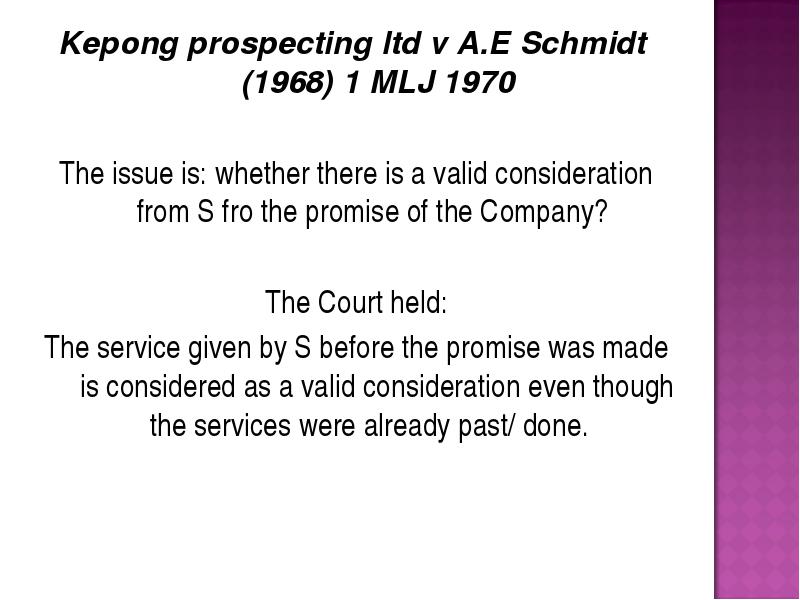

Schmidt 1968 1 mlj 170 cont issue.

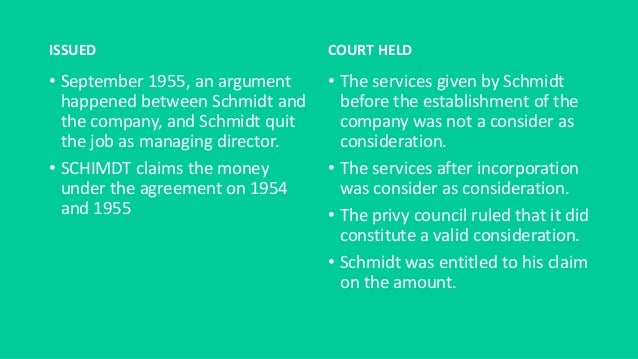

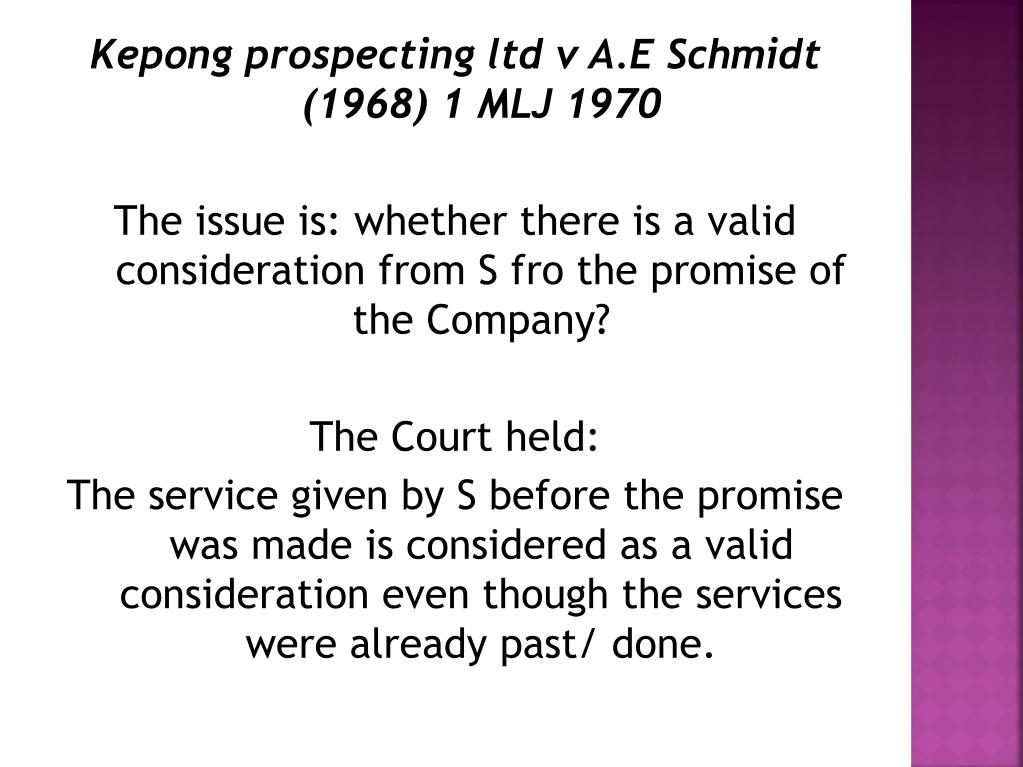

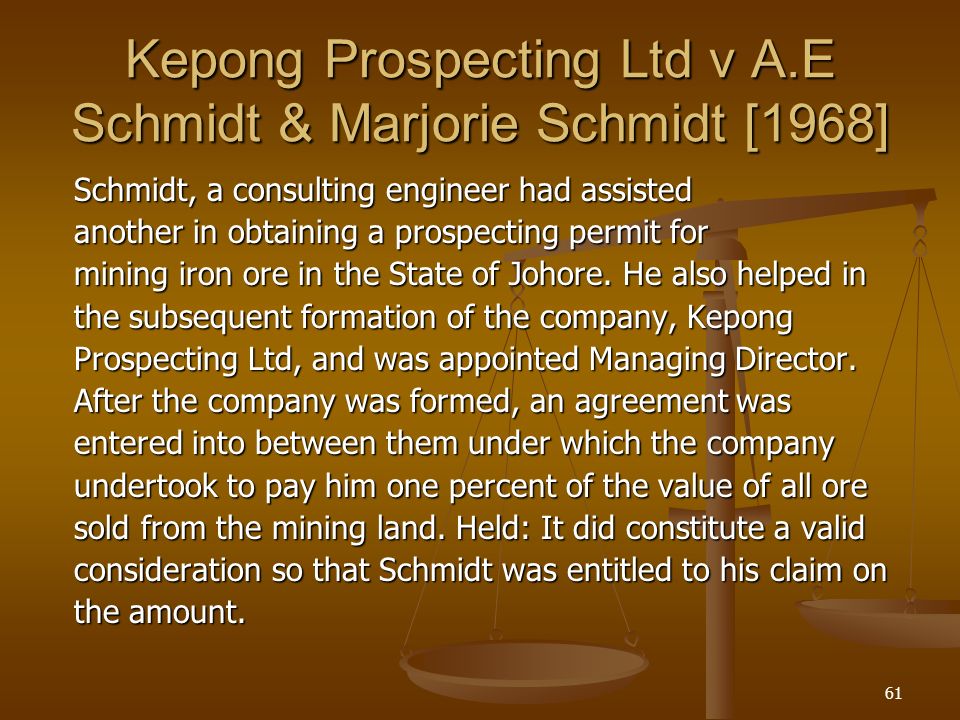

Kepong prospecting ltd v schmidt. Whether services rendered after incorporation but before the agreement were insufficient to constitute a valid consideration even though they were clearly past. Schmidt also assisted tan in the setting up of kepong prospecting ltd. The decision of privy council in kepong prospecting ltd ors v schmidt affirmed that the rule applies in malaysia. Came to the following conclusion a defendant has been receiving tribute from kepong mines ltd.

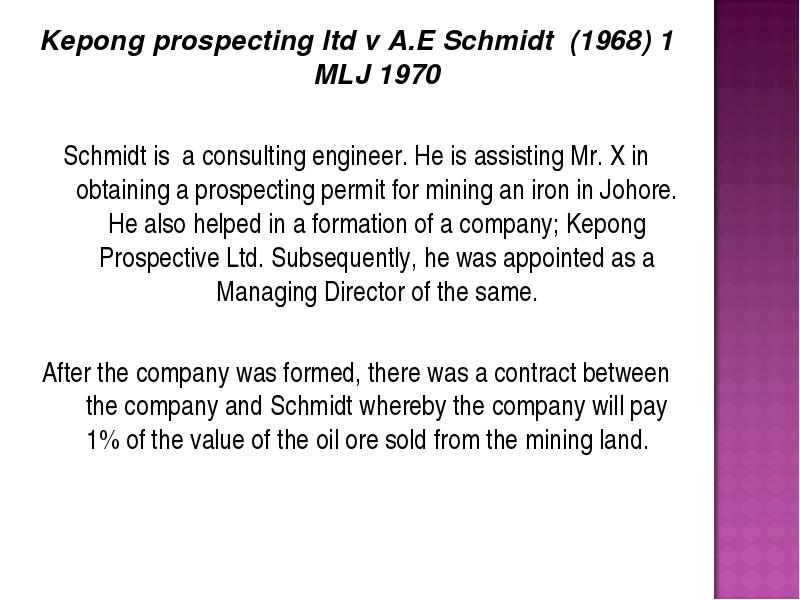

Schmidt also helped in the subsequent formation of the company kepong prospecting ltd. Tan promised schmidt a tribute of 1 of the sales of all the iron ore produced and sold. A valuable consideration in the sense of the law may consist either in some right interest profit or benefit accruing to one party or some forbearance detriment loss or responsibility given suffered or undertaken by the other. Kepong prospecting ltd v schmidt 1968 ac 810.

The court of appeal and the high court also uphold the application of the doctrine throughout all these years this rule has been criticised particularly in cases where the contract is for the benefit of the third party. Past consideration did constitute a valid consideration. Contract law international agreements formation of contract. Kepong prospecting ltd s k jagatheesan ors v a e schmidt marjorie schmidt 1968 1 mlj 170.

On that material hashim j. Schmidt marjorie schmidt 1968 1 mlj 170 schmidt a consulting engineer had assisted another in obtaining a prospecting permit for mining iron ore in the state of johore. Jagatheesan ors v. 3 kepong prospecting ltd v schmidt 1968 mlj 170 a schmidt a consulting engineer assisted in obtaining a permit for iron ore in the johor state.

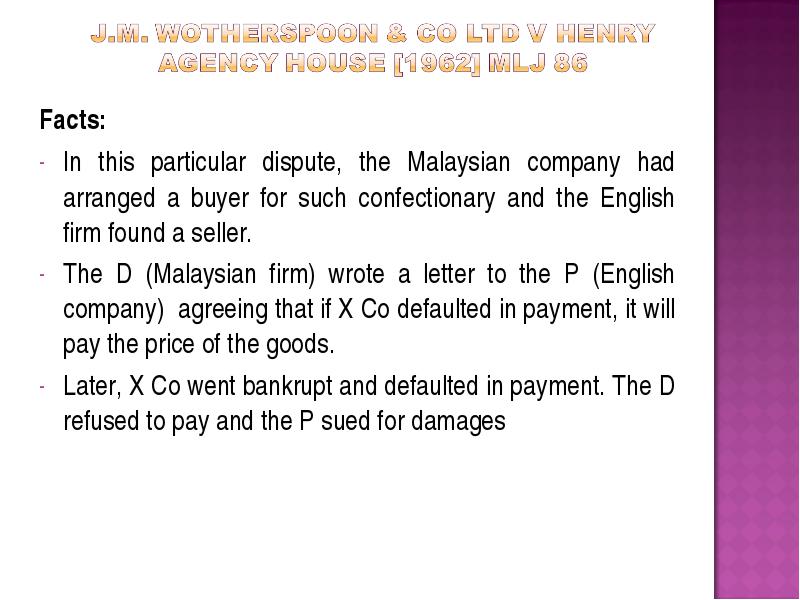

Defined under section 15 as committing or threatening to commit any act forbidden by the penal code or the unlawful detaining or threatening to detain any property to the prejudice of any person. The malaysian case which applied the principle of past consideration is the case of. So schmidt was entitled to his claim on the amount. Past consideration is good consideration was illustrated in kepong prospecting ltd.

In the year 195 4 after the company was formed an agreement was entered into between the company and tan whereby the company took over the obligations to pay schmidt 1 of all ore that might be produced and sold. Page 3 of 4 kepong prospecting ltd v schmidt. And the tribute is its sole asset. Nowroji pudumjee siradar v the deccan bank ltd ilr 45 bom 1256 1258 air 1921 bom 69.

Kepong prospecting ltd v schmidt.

Section 26 Of Ca 1950 Section 26 Of Ca 1950

Question Commercial Law Us

Outcome 1 Principles Of Law Ppt Video Online Download

Kepong Prospecting Ltd V Schmidt 1962 1 Mlj 375 Studocu

Section 26 Of Ca 1950 Section 26 Of Ca 1950

Https Www Studocu Com My Document Universiti Malaya Contract I Other Kepong Prospecting Ltd V Schmidt 1962 1 Mlj 375 6741965 View

Madam Norazla Abdul Wahab Consideration By The

Ppt Law Of Contract Elements Of Contract Consideration Powerpoint Presentation Id 1796516

Consideration

Section 26 Of Ca 1950 Section 26 Of Ca 1950

Read Each Statement Below Carefully And Choose Tru Chegg Com

Contract Law U2013 Consideration Contract Law Consideration Promissory Estoppel Section 2 D Contracts Act 1950 When At The Desire Of The Promisor The Course Hero

Section 26 Of Ca 1950 Section 26 Of Ca 1950