Section 127 Income Tax Act Malaysia

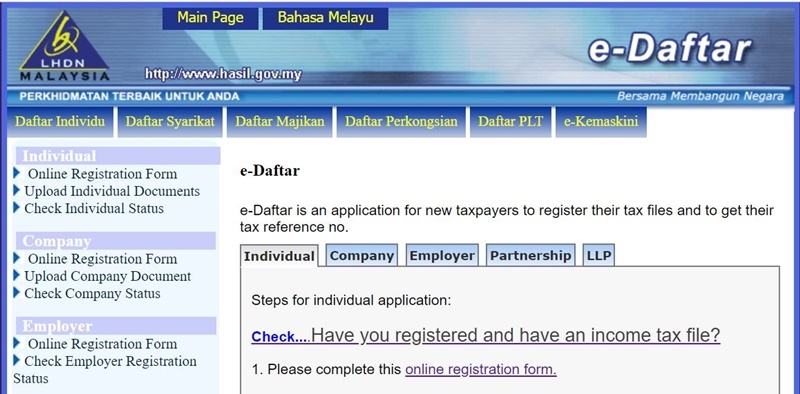

E Filing File Your Malaysia Income Tax Online Imoney

E Filing File Your Malaysia Income Tax Online Imoney

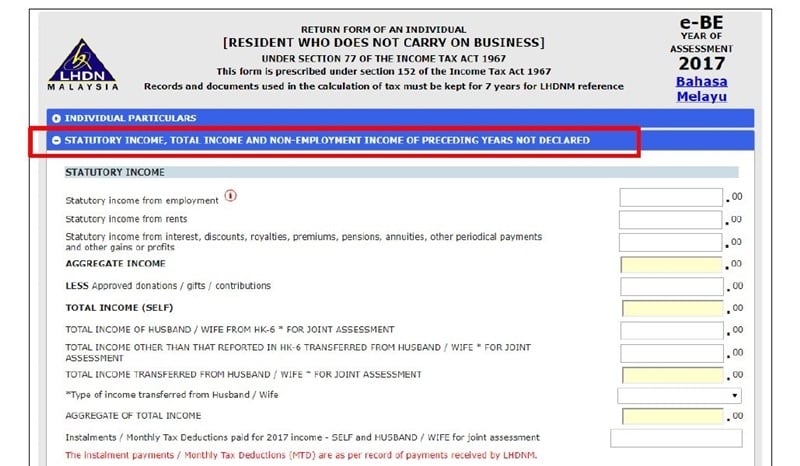

Malaysia Personal Income Tax Guide 2019 Ya 2018

Malaysia Personal Income Tax Guide 2019 Ya 2018

E Filing File Your Malaysia Income Tax Online Imoney

E Filing File Your Malaysia Income Tax Online Imoney

Non chargeability to tax in respect of offshore business activity 3 c.

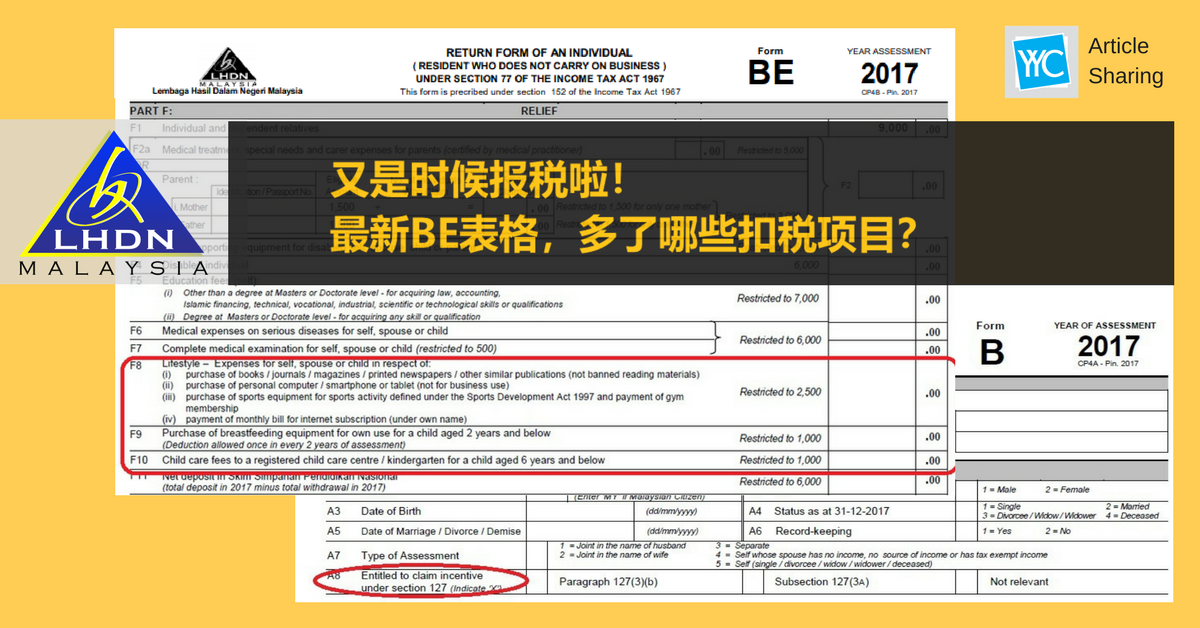

Section 127 income tax act malaysia. Incentive under section 127 refers to the income tax act 1976. Incentive under section 127 refers to the income tax act 1976. In the same page there is an item called entitled to claim incentive under section 127 which refers to claiming incentives under section 127 of the income tax act ita 1976. Akta cukai pendapatan 1967 is a malaysian laws which enacted for the imposition of income tax.

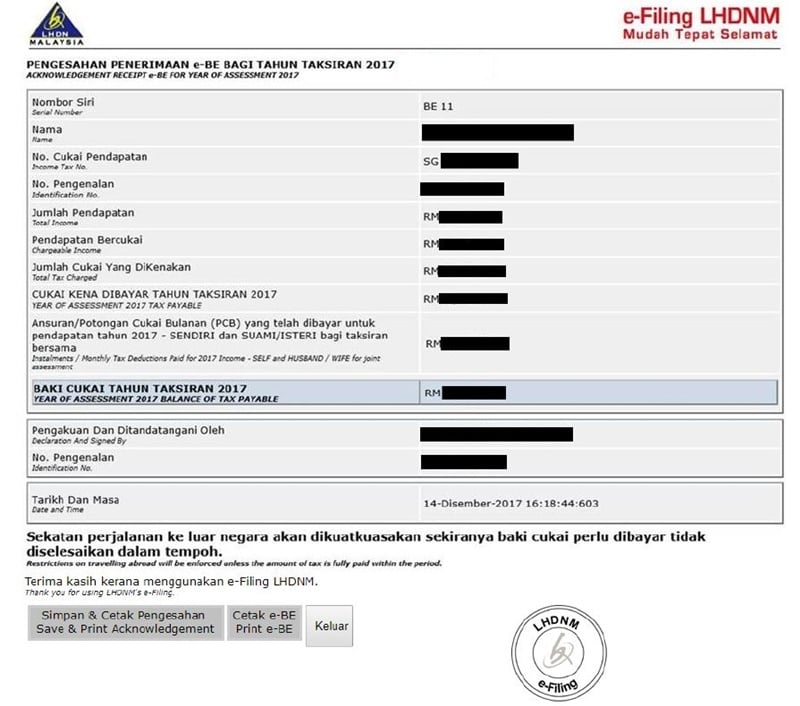

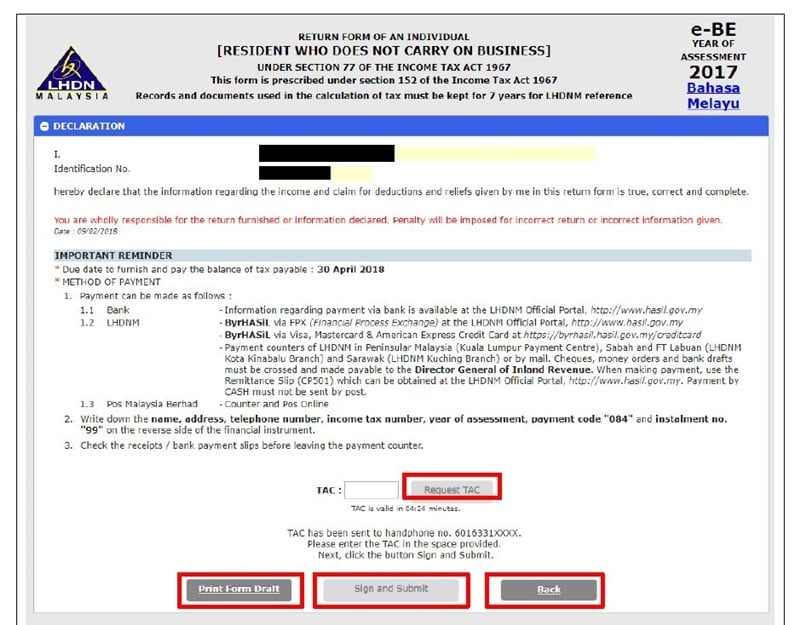

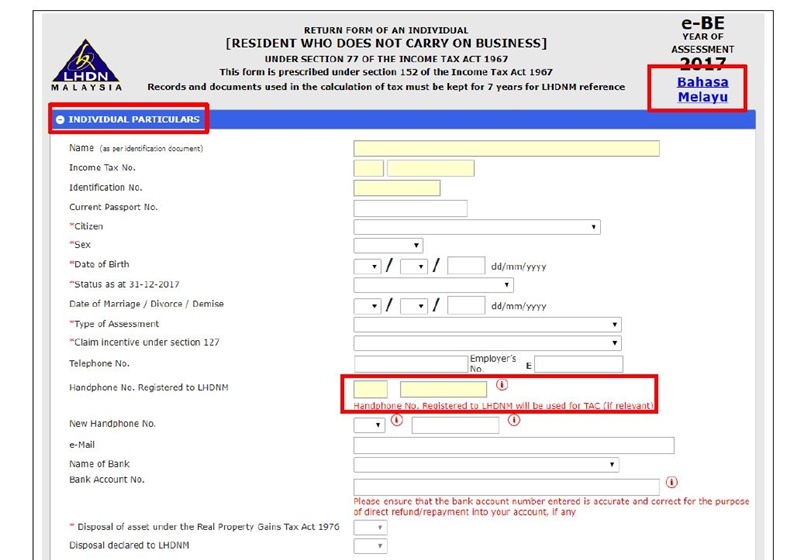

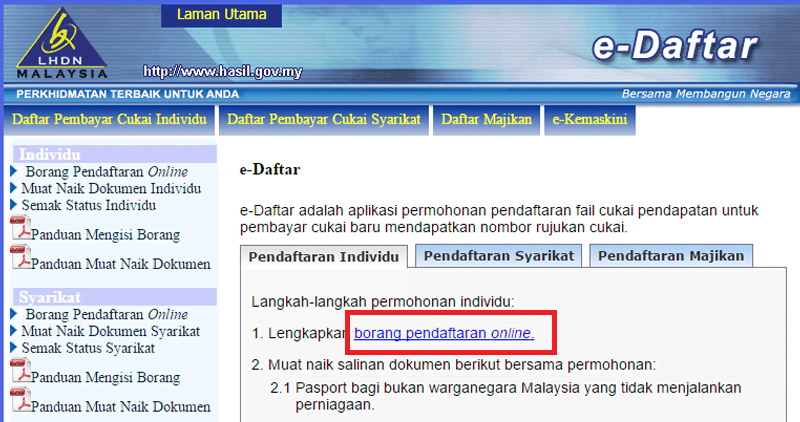

Section 127 provides that any income specified in part i of schedule 6 in the ita 1967 shall be exempt from tax. A tac which is needed to sign and submit your e form will be sent to your handphone number registered to lhdn so ensure it is correct. There will also be a layak menuntut insentif dibawah seksyen 127 which refers to claiming incentives under section 127 of the income tax act ita 1976. Section 127 of the income tax act 1967 ita is included in the mutual exclusion list of a gazette order the taxpayer therefore cannot make a claim for the incentive offered in the said gazette order.

Laws of malaysia act 53 income tax act 1967 arrangement of sections part i preliminary section 1. A tac which is needed to sign and submit your e form will be sent to your handphone number registered to lhdnm so ensure it is correct. Section 127 3a for tier 2 3 via an approval from the ministry of finance. Short title and commencement 2.

Charge of income tax 3 a. The general tax exemption provision is found in section 127 of the ita 1967. Some examples in this list of schedule 6 are the incomes of the government state government local authority co operative society limited liability partnership trade unions and others. This is incentives such as exemptions under the provision of paragraph 127 3 b or subsection 127 3a of ita 1976 which is claimable as per government gazette or with a minister s approval letter.

Following sections of the income tax act 1967. The revised guideline is available on mida s website www mida gov my resources forms and. It is only applicable to those who have incentives claimable as per government gazette or with a minister s approval letter. This is incentives such as exemptions under the provision of paragraph 127 3 b or subsection 127 3a of ita 1976 which is claimable as per government gazette or with a minister s approval letter.

An approved ohq company is eligible for income tax exemption for a period of 10 years under section 127 income tax act 1967 for income derived from the following sources. The income tax act 1967 malay. Business income income arising from services rendered by an ohq company to its offices or related companies. Interpretation part ii imposition and general characteristics of the tax 3.

Malaysia Personal Income Tax Guide 2019 Ya 2018

E Filing File Your Malaysia Income Tax Online Imoney

Malaysia Personal Income Tax Guide 2019 Ya 2018

E Filing File Your Malaysia Income Tax Online Imoney

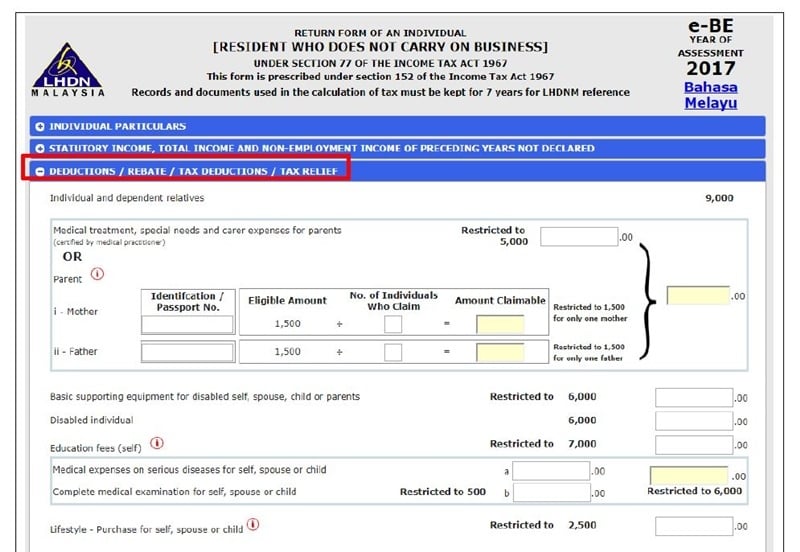

The Gobear Ultimate Guide To Lhdn Personal Income Tax E Filing Gobear Malaysia

E Filing File Your Malaysia Income Tax Online Imoney

Malaysia Personal Income Tax Guide 2019 Ya 2018

The Gobear Ultimate Guide To Lhdn Personal Income Tax E Filing Gobear Malaysia

Avoid 300 Lhdn S Tax Penalty Here S How To Declare Income Tax

Http Www Mida Gov My Env3 Uploads Incentivescompilation Mida 2013 Appigincenticesita Pdf

E Filing File Your Malaysia Income Tax Online Imoney

Http Www Mida Gov My Env3 Uploads Services Incentivessept2011 Pdf